Applying the New Accounting Guidance for Contributions

The contribution margin is different from the gross profit margin, the difference between sales revenue and the cost of goods sold. While contribution margins only count the variable costs, the gross profit margin includes all of the costs that a company incurs in order to make sales. The higher the percentage, the more of each sales dollar is available to pay fixed costs. To determine if the percentage is satisfactory, management would compare the result to previous periods, forecasted performance, contribution margin ratios of similar companies, or industry standards.

Company

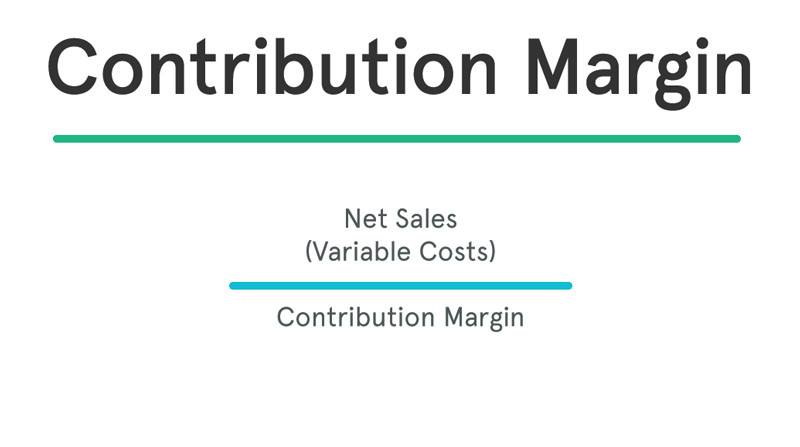

When the contribution margin is expressed as a percentage of sales, it is called the contribution margin ratio or profit-volume ratio (P/V ratio). Note that the total contribution of £180,000 is not the total profit made by the business. This is because we have not yet taken account of the fixed costs of the business.

Basic Concepts

Managers monitor a company’s sales volume to track whether it is sufficient to cover, and hopefully exceed, fixed costs for a period, such as a month. Contribution margin is the dollar sales amount available to apply (contribute) toward paying fixed costs during the period. In addition, whatever is left over after all fixed costs have been covered is profit, so contribution margin also contributes to profit—specifically, what we call operating income. An essential concept when dealing with contribution margins is whether a cost is fixed or variable. A fixed cost is any cost that is incurred in the same amount, irrespective of changes in transaction volume.

How Do You Calculate Contribution Margin?

- A low margin typically means that the company, product line, or department isn’t that profitable.

- Since machine and software costs are often depreciated or amortized, these costs tend to be the same or fixed, no matter the level of activity within a given relevant range.

- This pledge meets the definition of a contribution in that it is an unconditional transfer of cash that is both voluntary and nonreciprocal.

- While gross profit is more useful in identifying whether a product is profitable, contribution margin can be used to determine when a company will break even or how well it covers fixed costs.

- The contribution concept is usually referred to as contribution margin, which is the residual amount divided by revenues.

- It is important to note that this unit contribution margin can be calculated either in dollars or as a percentage.

In these examples, the contribution margin per unit was calculated in dollars per unit, but another way to calculate contribution margin is as a ratio (percentage). Recall that Building Blocks of Managerial Accounting explained the characteristics of fixed and variable costs and introduced the basics of cost behavior. Let’s now apply these behaviors contribution definition in accounting to the concept of contribution margin. The company will use this “margin” to cover fixed expenses and hopefully to provide a profit. The contribution margin measures how efficiently a company can produce products and maintain low levels of variable costs. It is considered a managerial ratio because companies rarely report margins to the public.

Contribution Margin: Definition, Overview, and How To Calculate

As we said earlier, variable costs have a direct relationship with production levels. However, ink pen production will be impossible without the manufacturing machine which comes at a fixed cost of $10,000. This cost of the machine represents a fixed cost (and not a variable cost) as its charges do not increase based on the units produced. Such fixed costs are not considered in the contribution margin calculations.

After all fixed costs have been covered, this provides an operating profit. Investors and analysts use the contribution margin to evaluate how efficient the company is at making profits. For example, analysts can calculate the margin per unit sold and use forecast estimates for the upcoming year to calculate the forecasted profit of the company. Contribution should be calculated using the accrual basis of accounting, so that all costs related to revenues are recognized in the same period as the revenues. Otherwise, the amount of expense recognized may incorrectly include costs not related to revenues, or not include costs that should be related to revenues.

If the company realizes a level of activity of more than 3,000 units, a profit will result; if less, a loss will be incurred. Gross profit is the dollar difference between net revenue and cost of goods sold. Gross margin is the percent of each sale that is residual and left over after the cost of goods sold is considered. The former is often stated as a whole number, while the latter is usually a percentage. 11 Financial is a registered investment adviser located in Lufkin, Texas. 11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements.

If the contribution margin for an ink pen is higher than that of a ball pen, the former will be given production preference owing to its higher profitability potential. Such decision-making is common to companies that manufacture a diversified portfolio of products, and management must allocate available resources in the most efficient manner to products with the highest profit potential. In our example, a ratio of 36.97% means that every dollar in sales contributes approximately $0.37 (thirty-seven cents) toward fixed costs. When using this measurement, be aware that the contribution margin does not account for the impact of a product on the bottleneck operation of a company. A low contribution margin may be entirely acceptable, as long as it requires little or no processing time by the bottleneck operation.